Table of Content

The October price was 0.3 percent higher than the $798,440 recorded last October and was the smallest year-over-year price gain in 29 months. October marked the fifth consecutive month with a single-digit annual price increase. With the average 30-year fixed mortgage rate expected to remain above 6.5 percent for the rest of the year, home prices will moderate further in the coming months as affordability remains a challenge.

Since interest payments play out over time, a buyer who plans to sell the home or refinance within a couple of years should probably skip the discount points and pay a higher interest rate for a while. If you took out a $300,000 home loan with a 30-year fixed rate of 5.5%, you’d pay around $313,000 in total interest over the life of the loan. The same loan size with a 15-year fixed rate of just 5.0% would cost only $127,000 in interest — saving you around $186,000 in total. If possible, give yourself a few months or even a year to improve your credit score before borrowing. You could save thousands of dollars through the life of the loan.

Best Savings Account Interest Rates of December 2022

In response to the Covid-19 pandemic, the Federal Reserve pumped money into the economy, spending trillions of dollars on mortgage-backed securities to help steer the U.S. away from another financial crisis. This move allowed lenders to offer rock-bottom interest rates, tumbling to the mid-2% range by the summer of 2021. Home loans are offered at both fixed and floating interest rates.

And while rates have been climbing steadily this year, they have a long way to go to hit the double digit returns of yesteryear. The average one-year CD has an APY of 0.52 percent, Bankrate’s July 27, 2022 rate survey data shows. Read on for smart tips on how to save enough money to buy a house and some mistakes to skip. It was then like a domino effect, taking down the mortgage industry, housing industry, and the economy as a whole.

Credit Card

Despite market turbulence, stock buybacks are on track to hit record levels by year-end. Finally, in the U.S., a strong dollar could weaken growth and lower inflation, serving as a mixed blessing for investors and consumers alike. When the U.S. dollar is strong it also makes U.S. assets pricier compared to foreign assets, which could impact the direction of capital flows. If the dollar remains strong, capital flows may be redirected away from America. One explanation suggests that higher capital accumulation could be a factor. Another suggests that modern welfare states, with their increased public spending, have as well.

Marco Santarelli is an investor, author, Inc. 5000 entrepreneur, and the founder of Norada Real Estate Investments – a nationwide provider of turnkey cash-flow investment property. His mission is to help 1 million people create wealth and passive income and put them on the path to financial freedom with real estate. He’s also the host of the top-rated podcast – Passive Real Estate Investing.

Real Estate Listings Showcase

Applicant’s CIBIL score, loan amount, employment type, income levels as well as the gender of the applicant are some of the factors that determine the rate of interest on your home loan application. If you are eligible for lower interest rates, not only should you grab it at the earliest. But also make sure the loan tenure is optimized to save you more. We’re transparent about how we are able to bring quality content, competitive rates, and useful tools to you by explaining how we make money. Be sure to ask your lender about the consequences of not closing within the timeframe specified in a rate lock agreement and also about what could happen if rates fall after you lock in a rate.

The fed funds rate has never been as high as it was in the 1980s. In another scenario, the buyer prioritizes a lower home price and purchases a $300,000 house instead. By buying a lower-priced home, they’ll be able to build equity faster, which will allow them to refinance more easily.

The central bank typically lowers the interest rate if the economy is slow and increases it if the economy expands too fast. The 10-year yield is so much lower than the two-year because investors have been buying long. The reason interest rates were so high in the 1980s was due to high inflation. With inflation, the cost of goods and services rises and your money doesn’t buy as much. And so, while savers enjoyed higher rates on their certificates of deposit, their spending power took a hit.

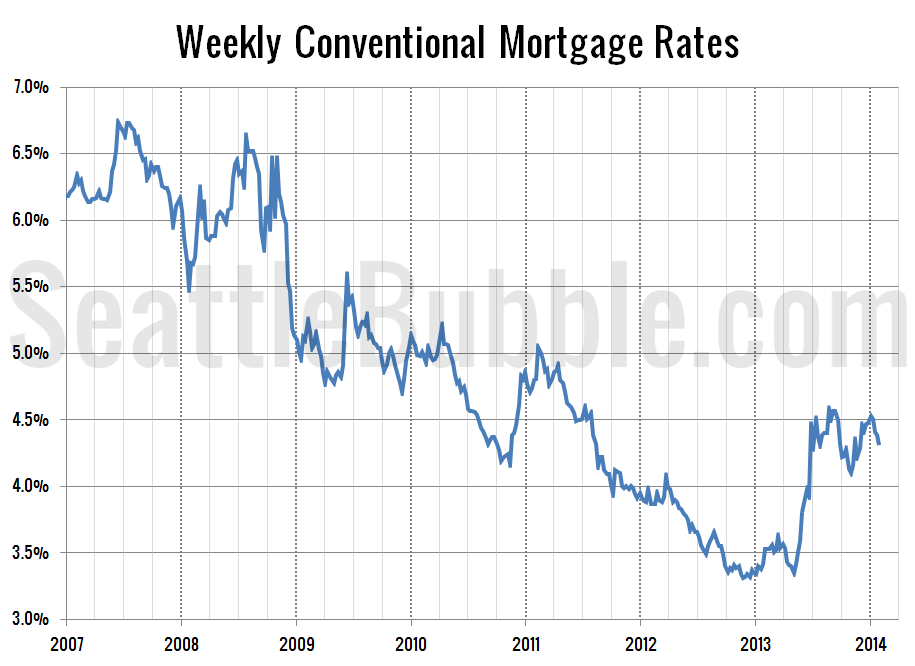

They continued to fall steadily and were in the mid-3% range by 2012. A big reason for this was that the bond market panicked a little bit when the Federal Reserve said it would stop buying as many bonds. Short-term rates, or the rates at which financial institutions borrow money, ended up being slashed to the point where they were at or near zero. This made it extremely cheap for banks to borrow funds so they could keep mortgage rates low. When mortgage interest rates slide, refinancing becomes more attractive to homeowners. The extra monthly savings could give you wiggle room in your budget to pay down other debt or boost your savings.

Other rates fell, too, as the central bank slashed its benchmark interest rate. The average yield on one-year CDs fell below 2 percent APY in 2002, Bankrate data shows. Interest rates were reduced to help jump-start the economy following the stock market bubble. “Inflation has been at a four-decade high, so the Fed must fight it with full force,” says Greg McBride, CFA, Bankrate chief financial analyst.

Officials did hike rates on April 19, 1994, at an emergency meeting due to inflation worries, and they cut borrowing costs at an unscheduled Oct. 15, 1998, gathering. Consumers are seeing the highest federal funds rate in more than a decade. Many lenders will accept down payments as low as 3%, but a lower down payment will come with a higher interest rate. “Demand is a major part of current inflation, with household savings rates and consumer spending that have been much stronger coming out of the 2020 pandemic than for households in the early 70s,” he says. Mortgage rates have fluctuated dramatically in the last 50 years of recorded data by Freddie Mac. And while rates have increased significantly this year, averaging more than 5%, it still pales in comparison to the spikes in the early 1980s when the 30-year fixed rate exceeded 18%.

No comments:

Post a Comment