Table of Content

The Depression kept interest rates low in the 1930s and during the war years of the 1940s, interest rates were pegged. It was only after the Treasury-Federal Reserve Accord of 1951 that the federal funds market emerged as the main market for U.S. banks to lend and borrow money from each other. Borrowers may be able to find a lower interest rate by shopping around rather than accepting the first loan offered. It is possible to reveal to each lender that another is offering a better rate as a negotiation tactic.

While we haven't seen the insanely high interest rates of the 1980s anymore, there's no predicting what they will do in the future. Mortgage rates depend on a large number of variables that can change at any given moment. There will be a lot of volatility over the next year, so make sure you’re saving adequately and planning for uncertainty when you can,” Kushi says. “This way Powell can continue with his agenda to slow the economy down but help create a softer landing, a more moderate recessionary environment,” Poljak says.

Charted: The Rise of Stock Buybacks Over 20 Years

After an eight-month recession beginning in August 1990, Greenspan and Co. managed to take the fed funds rate all the way up to a target level of 6.5 percent in May 2000, the highest of the period. Rates reached a low of 3 percent in September 1992, the lowest of the decade. At the end of the day, it comes down to your goals and priorities as a buyer. Are you focused on buying a bigger home, or is your goal to keep your monthly payment as low as possible?

Therefore, the rate and payment results you see from this calculator may not reflect your actual situation. You may still qualify for a loan even in your situation doesn’t match our assumptions. To get more accurate and personalized results, please call to talk to one of our mortgage experts. If you’ve recently entered the housing market, you’ve probably developed a sudden passion for interest rates. This may be particularly true for mortgage loan rates, a topic you’ve probably given little thought to in the past. Bankrate follows a strict editorial policy, so you can trust that our content is honest and accurate.

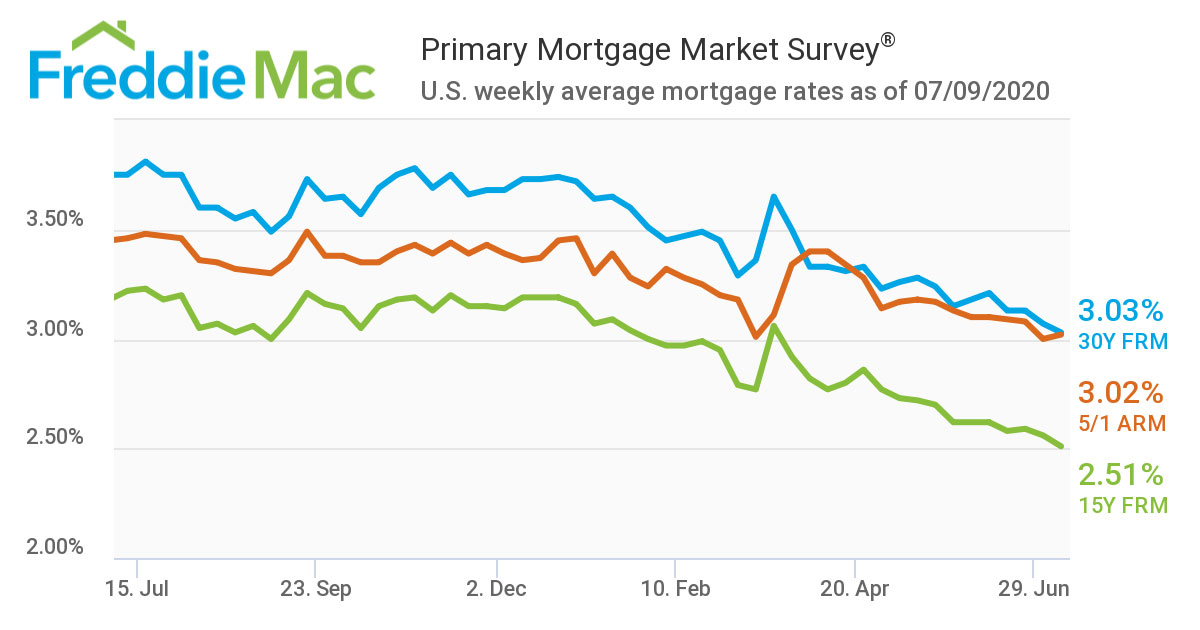

Mortgage rate trends in the 2010s

The agency anticipates 2022 short-term interest rates to rise substantially. In 2022, long-term interest rates are predicted to rise significantly from their 2021 lows. After 2022, CBO forecasts short- and long-term interest rates to climb slower. Mortgage rates then hovered within the same range throughout 2021, but since July 2022, the Fed has been raising its rates to reduce the amount of money in the economy.

Then it fell 4% through Nov. 3, as shorter-term investors woke up to reality. Then the policy pivot-talk pattern repeated, with the index rising 4% from Nov 3. Through Dec. 13, before the FOMC announcement and Powell press conference on Dec. 14 helped set up a two-day decline of 2%. There has been much discussion about a slowing housing market in recent months.

Mortgage Rates Forecast For 2023: Will Rates Drop?

As house prices start to rise, your required down payment will go up as well. After the housing crisis, which caused an estimated six million people to lose their homes to foreclosure, mortgage rates stayed low. For years following the crisis, home prices declined through early 2012 and then slowly began to rise.

Loan specifics—Longer repayment terms can increase the interest rate because it is riskier for lenders. In addition, making too low a down payment can result in the borrower receiving a higher interest rate. Choosing a shorter loan term and putting more money down can lower the interest rate a borrower is subject to. There are many factors that affect what interest rates people get on their mortgages and auto loans.

Still, relative to many of the other major global currencies it remains strong. Along with this, rates usually have cycles that last between 22 and 27 years. When cycles shift from rising to falling rates, a quick reversal typically takes place. This was seen in 1982, when interest rates dropped 25%—from 14.2% to 10.4%—in one year.

For example, with a credit score of 580 you may qualify only for a government-backed loan such as an FHA mortgage. FHA loans have low interest rates, but come with mortgage insurance no matter how much money you put down. Most mortgages, including FHA loans, require at least 3 or 3.5% down.

Although some banks, like online institutions, give depositors interest on checking accounts, most do not. Banks that do pay interest on checking accounts don't tend to pay a lot. In 2010 the typical interest rate for a checking account was 0.11 percent and it has steadily declined to today's rate of 0.04 percent.

The statewide Unsold Inventory Index increased to 3.3 months in October 2022 from 2.9 months recorded in the prior month and from 1.8 months recorded in the same period a year ago. Home sales have been on a downward trend for 16 straight months on a year-over-year basis. It was the third time in the last four months that sales dropped more than 30 percent from the year-ago level. The monthly 10.4 percent sales decline was worse than the long-run average of +0.5 percent change recorded between September and October in the past 43 years. Sales in all price segments continued to drop by 30 percent or more year-over-year, with the $750,000-$999,000 price segment falling the most at 40.8 percent. The high-end market ($1 million-$1,999,000) experienced the smallest sales drop at 34.1 percent.

While big increases in CD yields are encouraging to savers, high inflation tempers their enthusiasm. “CD yields fell to new record lows when interest rates were slashed to near-zero levels in the early stages of the pandemic,” says McBride. From June 2020 to June 2021, the average five-year CD fell to 0.31 percent APY from 0.58 percent APY. From June 2020 to June 2021, the average one-year CD dropped to 0.17 percent APY from 0.4 percent APY.

In 2020, the Federal Reserve lowered rates in response to COVID-19 Now, with prices rising across the economy because of numerous factors, the Fed is hiking its discount rate to cool inflation. Mortgage points represent a percentage of an underlying loan amountâone point equals 1% of the loan amount. Less than a year ago, mortgage rates were at or near historic lows. This year, due to both higher prices and mortgage rates that are hovering around 7%, a typical buyer is facing a $2,065 monthly payment.

The higher the interest rate, the less attractive the opportunity to borrow money at that rate is for you as a homebuyer. As a result, it could make more sense to borrow at a lower rate, especially if you have a modest amount to spend on a home and are looking for a low-interest loan. Accordingly, in CBO’s projections, the 3-month Treasury bill rate will fall to 2.4 percent by the fourth quarter of 2026. In 2022, CBO expects inflation to remain high due to factors that keep supply growing slower than demand in product and labor markets. CBO expects inflation to exceed the Fed's 2 percent long-term goal in 2023 before approaching it in 2024.

For instance, average expenditures of total GDP in the UK averaged 35% between 1981 and 1960, compared to 8% between 1700 and 1750. While the exact reasons are unclear, broad structural forces may be influencing interest rates. Interest rates in the 18th and 19th centuries also provide illuminating trends. U.S. interest rates will stay near zero for at least three years as the Federal Reserve enacts measures to prop up the economy. Email The Credible Money Expert at and your question might be answered by Credible in our Money Expert column. Keeping a close watch will make it easier to find and lock in a better rate.

No comments:

Post a Comment